The B2B digital solutions specialist

The B2B digital solutions specialist

Open Banking allows wholesalers to accept payment by bank transfer and is an extremely secure means of payment, offering two principal advantages compared to debit, credit or corporate credit cards.

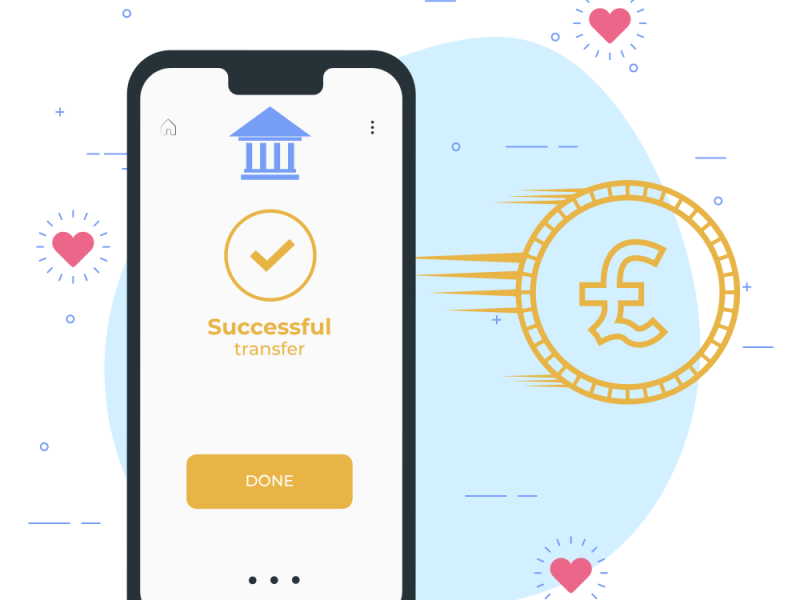

Firstly, it’s much cheaper when compared to the cost associated with processing payments from a card, but secondly, payments are received more quickly, with payments arriving in your bank account within seconds – compared to two-to-four days for card payments.

It can be incorporated into various areas of your business, offering an enhanced audit trail of when a payment is made and by whom. Payments can be associated with specific invoices, reducing the overheads associated with reconciling accounts, while finance teams can be notified via email when payments have been made, by whom, and to which invoice it relates, further reducing costs. For wholesale businesses, Open Banking adds most value as a replacement for card payments.

Implementing open banking to your digital channel is relatively straightforward. You will need an accounts section within your eCommerce where customers can see what they owe and view previous invoices.

Once these features are enabled, wholesalers can integrate an Open Banking capability that allows your customers to pay off a balance or invoice. Enhanced functionality can be introduced, such as deploying the ability to pay off multiple invoices.

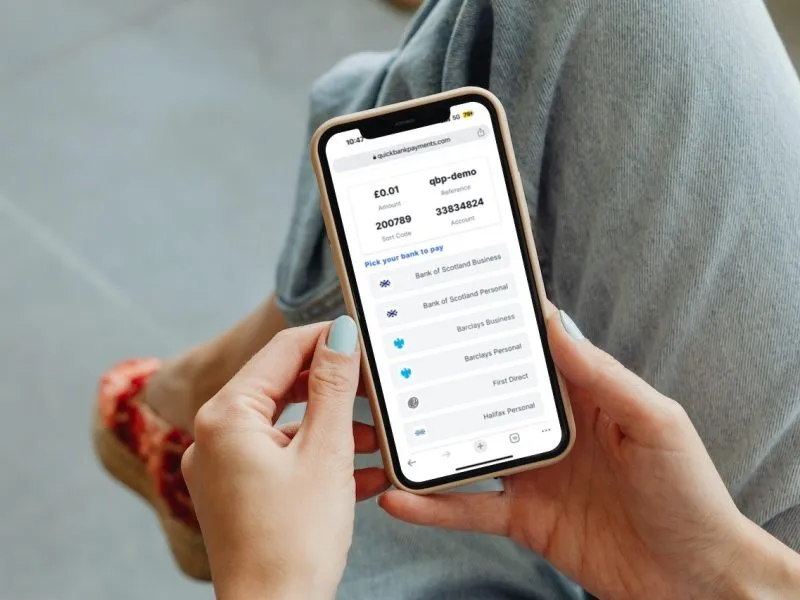

A QR code can be automatically added to customers’ invoices. When customers scan the QR code, their banking app automatically opens with the value of the invoice auto-populating the screen, along with the recipient’s banking details. All your customer has to do is click ‘send’ and the money arrives in your account.

In parallel, your accounts team receive an email stating that monies have been received, who the sender is and which invoice the payment relates to.

Accepting payments in depot at the point of delivery becomes more challenging as they are processed in real time and often in full view of other customers.

A real-time connection is required between your Open Banking solution and your bank, meaning that as soon as the payment has landed, your staff are notified that the transaction is complete. b2b.store advocates carefully deployed pilots of Open Banking into these live environments.

This process is often slow and clunky, managed by internal resources and with the added challenge if the majority of the payments being made on account.

With Open Banking, requests for payment are incorporated to automated digital notifications sent to your customers based on the specific payment terms of an invoice or account.

Offices 13 B & C, Innovation Centre, Warwick CV34 6UW, UK

Email: hello@b2b.store • Tel: +44 (0)1926 298867

© 2026 B2B Store • Company No. 03956929